Amendments for the 2022 Valuation Manual

for the Consideration of

the Life Insurance and Annuities (A) Committee

July 19, 2021

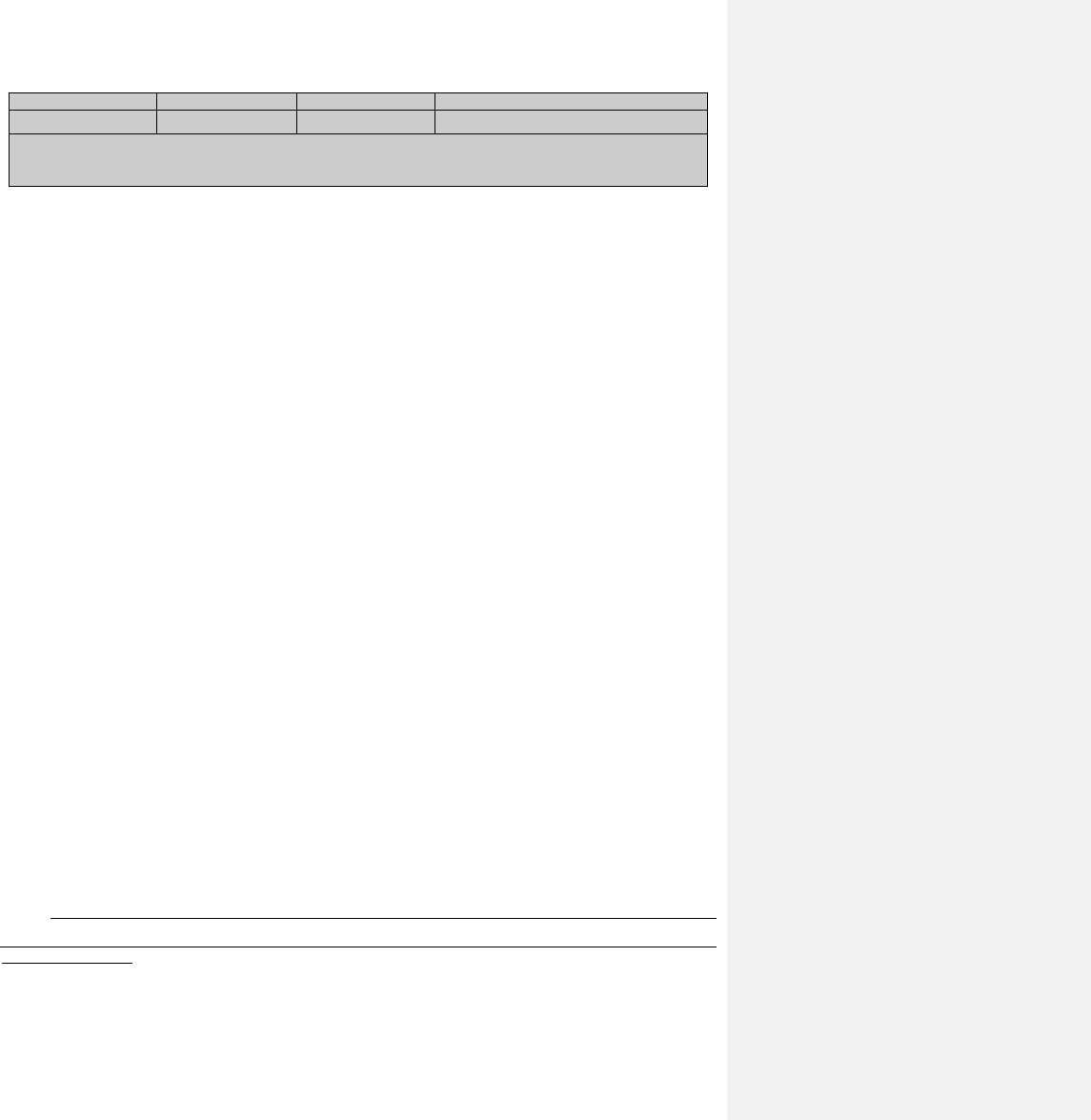

Attachment

Number

Page

Number

LATF VM

Amendment

Valuation Manual

Reference

Valuation Manual Amendment Proposal Descriptions

LATF

Adoption

Date

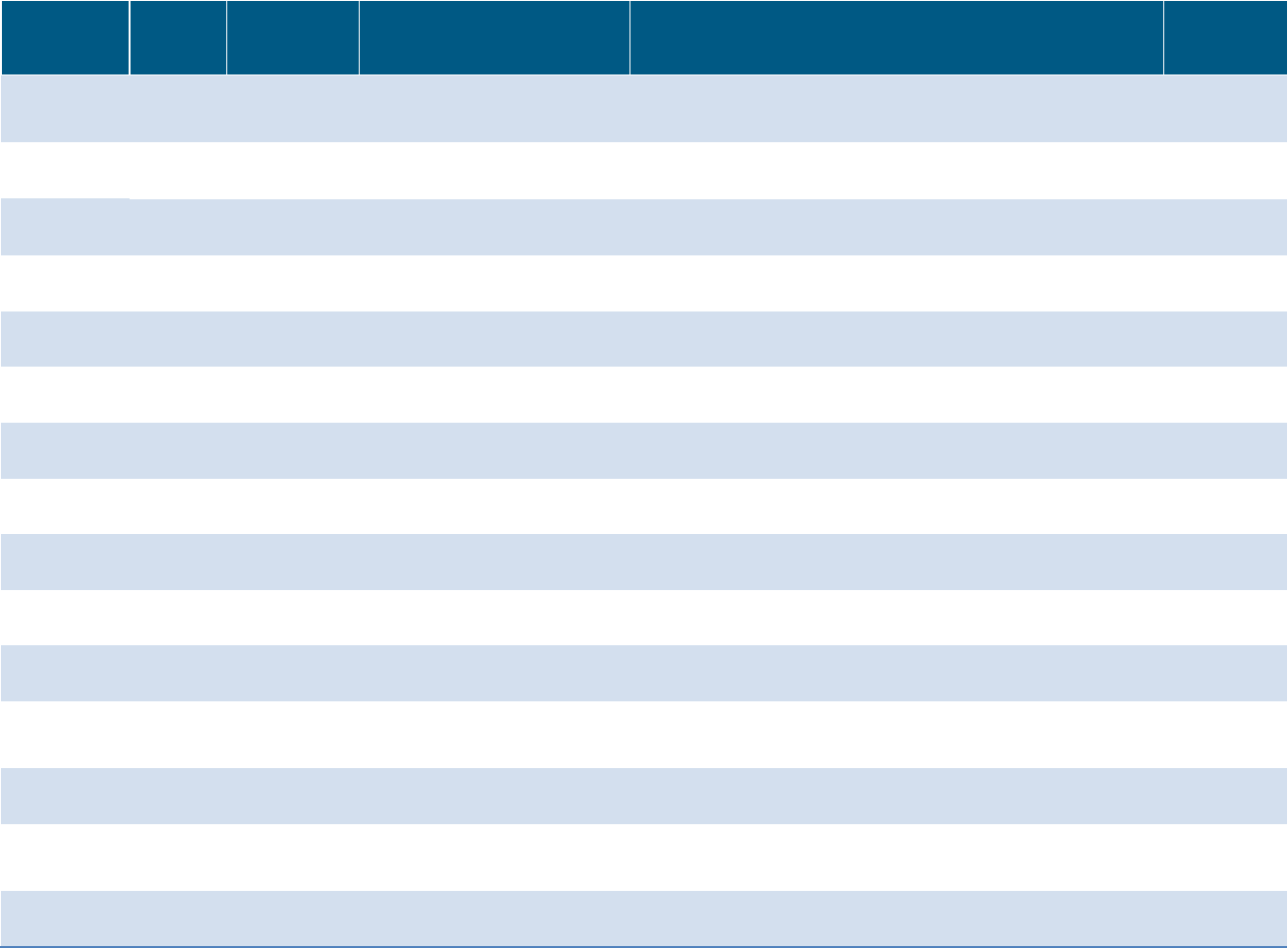

1

3

2019-33

Sect II, VM-20, VM-51

Clarify the definition of individually underwritten life insurance

and the applicability of PBR requirements for group contracts

with individual risk selection issued under insurance certificates.

7/1/2021

2

11

2020-02

VM-20 Section 2.H and new

Section 2.I

Provide clearer guidance on the boundaries of a company’s

latitude in following VM-20 steps

10/29/2020

3

15

2020-03

VM-20 Section 3.B.3

Clarify NPR calculation requirements

8/27/2020

4

19

2020-08

VM-20 Section 9.C.2.d.vi.

Clarify and introduce a third permissible technique for the

calculation of company experience rates.

12/3/2020

5

22

2020-09

VM Section II, Subsection 1.D

Modify Life PBR Exemption

11/5/2020

6

25

2020-10

VM-20, VM-31

Mortality improvement

6/10/2021

7

35

2020-11

VM Section II, Subsection

1.D.4

Modify Life PBR Exemption-Part 2

2/11/2021

8

37

2020-13

VM-20, Sec 7.D.3

Asset Collar

4/8/2021

9

38

2021-03

VM-21, Section 6.C.5:

Update the reference to required minimum distribution age

5/6/2021

10

41

2021-04

VM-02 Section 3.A

Clarify the language in the previously adopted edits to VM-02 to

avoid any potential circularity.

4/29/2021

11

43

2021-05

VM-01,VM-20 7.E,VM-21

4.D, VM-31 3.D.6, 3.F.6

Clarify modeled company investment strategy and comparison to

the alternative investment strategy

5/20/2021

12

48

2021-06

VM-50, VM-51

Revise VM-50 and VM-51 to allow experience reporting a

reinsurer or third-party administrator and a correction to VM-51

Appendix 4

5/27/2021

13

91

2021-07

VM-20 Section 2.A.3, 3.A, 3.B

3.C and 6.B

Clarify ULSG NPR Calculation Requirements

6/24/2021

14

99

2021-09

VM-21 Section 1.E (new), 3.H

(new), VM-31 Section 3.E.1,

3.F.2.e

Update VM-31 materiality language to be consistent new section

of VM-21 addressing materiality.

7/1/2021

15

102

2021-10

VM 51 App 4

Remove "at issue" from Smoker Status data element name to

allow for use of the smoker status at the time of data submission

6/24/2021

W:\National Meetings\2021\Summer\TF\LA\Adoptions\Documents for the A Committee\VM chart for A Committee 07_19_21.docx

© 2010 National Association of Insurance Commissioners 1

Life Actuarial (A) Task Force/ Health Actuarial (B) Task Force

Amendment Proposal Form*

1. Identify yourself, your affiliation and a very brief description (title) of the issue.

American Academy of Actuaries, Life Reserves Work Group

Addition of language to clarify the definition of individually underwritten life insurance and the

applicability of Principle-Based Reserve (PBR) requirements for group insurance contracts with individual

risk selection issued under insurance certificates.

2. Identify the document, including the date if the document is “released for comment,” and the location in

the document where the amendment is proposed:

January 1, 2021, version of the Valuation Manual, with the revisions to APF 2020-11 (adopted by LATF

on 2/11/21) shown in blue text.

3. Show what changes are needed by providing a red-line version of the original verbiage with deletions and

identify the verbiage to be deleted, inserted or changed by providing a red-line (turn on “track changes” in

Word®) version of the verbiage. (You may do this through an attachment.)

See Appendix

All proposed changes specific to this amendment proposal are shown in red text.

4. State the reason for the proposed amendment? (You may do this through an attachment.)

Individual insurance certificates issued under a group contract which utilize an individual risk selection

process, pricing, premium rate structures and product features are similar to individual life insurance

policies. They are currently excluded from VM-20 because they are filed under a group contract, but they

should be subject to VM-20 due to this similarity. See Appendix.

* This form is not intended for minor corrections, such as formatting, grammar, cross–references or spelling. Those

types of changes do not require action by the entire group and may be submitted via letter or email to the NAIC

staff support person for the NAIC group where the document originated.

NAIC Staff Comments:

Dates: Received

Reviewed by Staff

Distributed

Considered

3/19/19

Notes: APF 2019-33

W:\National Meetings\2010\...\TF\LHA\

© 2021 National Association of Insurance Commissioners

3

© 2010 National Association of Insurance Commissioners 2

Appendix

Issue

Certain contracts issued under a master group contract require individual risk selection in order to qualify for

issuance of the group insurance certificate; the certificates have similar acquisition approaches, provisions,

certificate-holder rights, pricing, and risk classification; and they are managed in a similar manner as individual

ordinary life insurance contracts. These individual certificates should follow the same reserve requirements as other

individual life contracts of the same product type. Therefore, a change is needed within the Valuation Manual to

bring these individual certificates into scope of VM-20.

Six changes are recommended:

1) Within the Reserve Requirements section (Section II), change the minimum reserve requirements to also

apply to group life contracts which, other than the difference between issuing a policy and issuing a group

certificate, have the same or mostly similar contract provisions, risk selection process, and underwriting as

individual ordinary life contracts (Section II, subsection 1.D);

2) Within the Reserve Requirements section (Section II), add a transition period for individual group

certificates issued on or before 1/1/2024 (Section II, subsections 1.F.1 and 1.F.2);

3) Within the Reserve Requirements section (Section II), add language and guidance note to subsection 1.G

and the corresponding footnote to include premiums from group life contracts which have individual

certificates that were issued using individual risk selection processes (Section II, subsection 1.G.1, footnote,

and guidance note) and to clarify the Calculation for Exemption (Section II, subsection 1.G.2). Comment

notes need to refer to NAIC Blanks (E) Working Group to update the PBR Supplement;

4) Add new paragraph, VM-20 Section 1.B (and reformat to make current paragraph Section 1.A) to clarify

group life certificates issued using individual risk selection processes, including a definition and

requirements to be met, are subject to the requirements of VM-20;

5) Add guidance note after first sentence in VM-20 Section 2.A.1 that group life certificates that meet the

definition for individual risk selection process use the same VM-20 Reserving Categories as defined in

Section 2;

6) Draft referral to the NAIC Blanks (E) Working Group to revise the VM-20 Reserves Supplement, Part 2 to

report premiums for total Group Life and Group Life with certificates subjected to an individual risk

selection process and which meet all of the conditions as defined in VM-20 Section 1.B separately.

© 2021 National Association of Insurance Commissioners

4

© 2010 National Association of Insurance Commissioners 3

VM Changes 1, 2 and 3 – II. Reserve Requirements

II. Reserve Requirements

This section provides the minimum reserve requirements by type of product, as set forth in the seven subsections

below, as follows:

(1) Life Insurance Products

(2) Annuity Products

(3) Deposit-Type Contracts

(4) Health Insurance Products

(5) Credit Life and Disability Products

(6) Riders and Supplemental Benefits

(7) Claim Reserves

All reserve requirements provided by this section relate to business issued on or after the operative date of the

Valuation Manual. All reserves must be developed in a manner consistent with the requirements and concepts

stated in the Overview of Reserve Concepts in Section I of the Valuation Manual.

Subsection 1: Life Insurance Products

A. This subsection establishes reserve requirements for all contracts issued on and after the operative date of

the Valuation Manual that are classified as life contracts as defined in SSAP No. 50 in the AP&P Manual,

with the exception of annuity contracts and credit life contracts. Minimum reserve requirements for

annuity contracts and credit life contracts are provided below in subsection 2 and subsection 5,

respectively.

B. Minimum reserve requirements for variable and nonvariable individual life contracts—excluding

guaranteed issue life contracts, preneed life contracts, industrial life contracts, and policies of companies

exempt pursuant to the life PBR exemption in in paragraph D below—subsection 1.G are provided by

VM-20, Requirements for Principle-Based Reserves for Life Products, except for election of the transition

period in

paragraph C below subsection 1.F.2 below. For this purpose, joint life policies are considered

individual life.

C. Minimum reserve requirements of VM-20 are considered principle-based valuation requirements for

purposes of the Valuation Manual.

D. Minimum reserve requirements for individual certificates under group life contracts (regardless of the

issue date of the master group life contract) which meet all the requirements in VM-20 Section 1.B are

provided by VM-20, except for election of the transition period in subsection 1.F.1 below.

E. Minimum reserve requirements for life contracts not subject to VM-20 are those pursuant to applicable

requirements in VM-A and VM-C. For guaranteed issue life contracts issued after Dec. 31, 2018, mortality

tables are defined in VM Appendix M, Mortality Tables (VM-M), and the same table shall be used for

reserve requirements as is used for minimum nonforfeiture requirements as defined in VM-02, Minimum

Nonforfeiture Mortality and Interest.

Guidance Note: The terms “policies” and “contracts” are used interchangeably.

© 2021 National Association of Insurance Commissioners

5

© 2010 National Association of Insurance Commissioners 4

F. A company may elect to establish minimum reserves pursuant to applicable requirements in VM-A and

VM-C for:

1. Business described in subsection 1.D above and issued on or after the operative date of the Valuation

Manual and prior to 1/1/2024.

2. Business not described subsection 1.D otherwise subject to VM-20 requirements and issued during

the first three years following the operative date of the Valuation Manual.

A company electing to establish reserves using the requirements of VM-A and VM-C may elect to use the

2017 Commissioners’ Standard Ordinary (CSO) Tables as the mortality standard following the conditions

outlined in VM-20 Section 3. If a company during the three years elects to apply VM-20 to a block of such

business, then a company must continue to apply the requirements of VM-20 for future issues of this business.

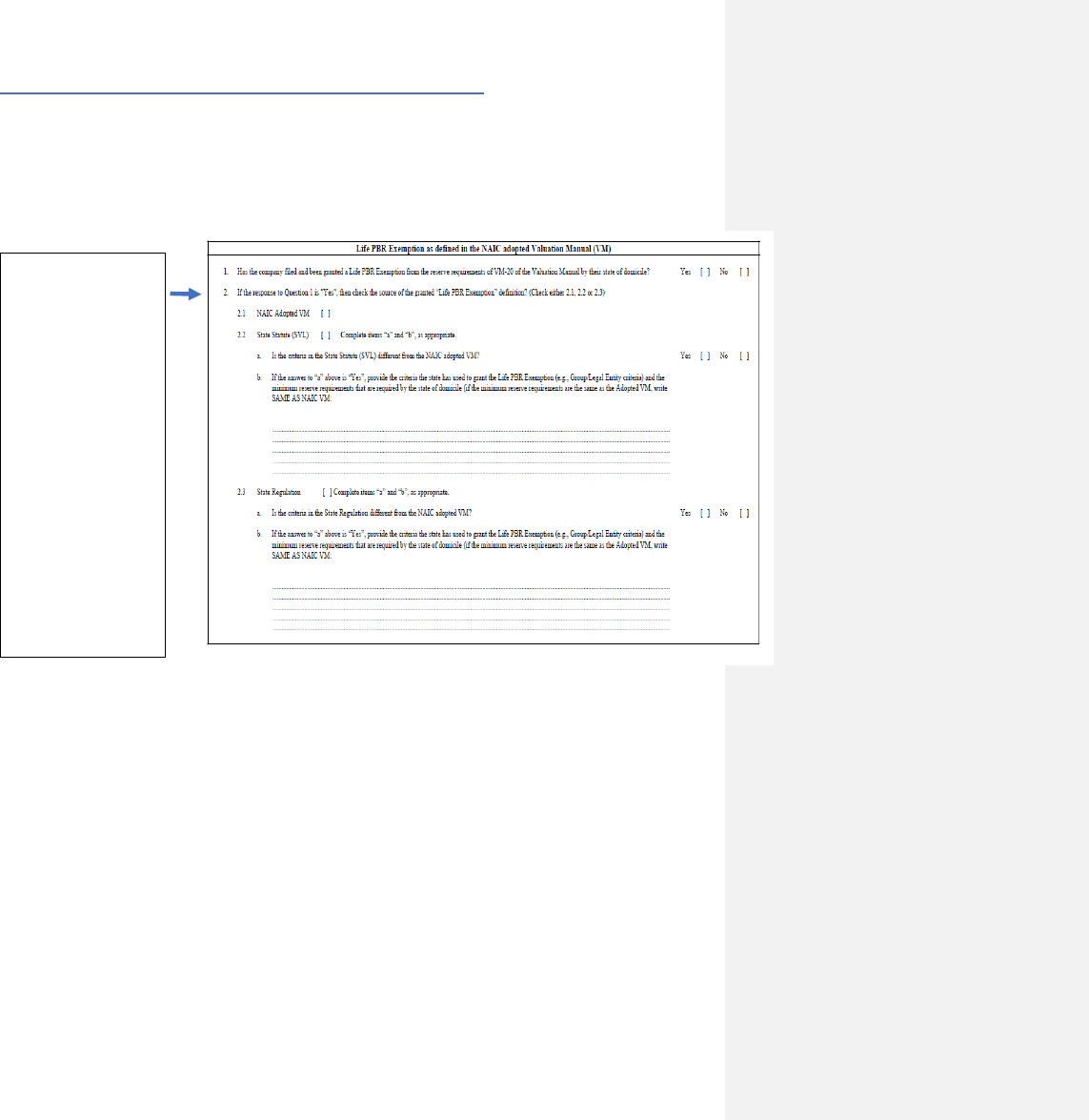

G. Life PBR Exemption

1. A company meeting the at least one of the conditions in Dsubsection 1.G.2 below may file a statement

of exemption for individual ordinary life insurance policies or certificates, except for policies or

certificates in Dsubsection 1.G.3 below, issued directly or assumed during the current calendar year,

that would otherwise be subject to VM-20. If a company has no business issued directly or assumed

during the current calendar year that would otherwise be subject to VM-20, a statement of exemption

is not required. For a filed statement of exemption, the statement must be filed with the domiciliary

commissioner prior to July 1 of that year certifying that at least one of the two conditions in Dsubsection

1.G.2 was met and the statement of exemption must also be included with the NAIC filing for the

second quarter of that year.

The domiciliary commissioner may reject such statement prior to September 1 and require the company

to follow the requirements of VM-20 for the ordinary life policies or certificates covered by the

statement.

If a filed statement of exemption is not rejected by the domiciliary commissioner, the filing of

subsequent statements of exemption is not required as long as the company continues to qualify for the

exemption; rather, ongoing statements of exemption for each new calendar year will be deemed to not

be rejected, unless: 1) the company does not meet either condition in D. subsection 1.G.2 below, 2) the

policies or certificates contain those in D. subsection 1.G.3 below, or 3) the domiciliary commissioner

contacts the company prior to Sept. 1 and notifies them that the statement of exemption is rejected. If

any of these three events occur, then the statement of exemption for the current calendar year is rejected

and a new statement of exemption must be filed and not rejected in order for the company to exempt

additional policies or certificates. In the case of an ongoing statement of exemption, rather than include

a statement of exemption with the NAIC filing for the second quarter of that year, the company should

enter “SEE EXPLANATION” in response to the Life PBR Exemption supplemental interrogatory and

provide as an explanation that the company is utilizing an ongoing statement of exemption.

2. Condition for Exemption:

a. The company has less than $300 million of ordinary lifeexemption premiums

1

, and if the company

is a member of an NAIC group of life insurerswhich includes other life insurance companies, the group

has combined ordinary lifeexemption premiums

1

of less than $600 million; or

The only new policies or certificates that would otherwise be subject to VM-20 being issued or assumed

by the company are due to election of policy benefits or features from existing policies or certificates

valued under VM-A and VM-C and the company was exempted from, or otherwise not subject to, the

requirements of VM-20 in the prior year.

Exemption premium is determined as follows:

Deleted: and

Deleted: Such a

Deleted: the

Deleted: of

Deleted: based on premiums from the prior calendar year

annual statement.

Deleted: T

Deleted: ¶

Deleted: .

© 2021 National Association of Insurance Commissioners

6

© 2010 National Association of Insurance Commissioners 5

a. The amount reported in the prior calendar year life/health annual statement, Exhibit 1, Part 1,

Column 3 (“Ordinary Life Insurance”), line 20.1; plus

b. The portion of the amount in the prior calendar year life/health annual statement, Exhibit 1, Part 1,

Column 3 (“Ordinary Life Insurance”), line 20.2 assumed from unaffiliated companies; minus

c. Amounts included in either (a) or (b) that are associated with guaranteed issue insurance policies

and/or preneed life insurance policies; minus

d. Amounts included in either (a) or (b) that represent transfers of reserves in force as of the effective

date of a reinsurance assumed transaction; plus

e. Amounts of premium for individual life certificates issued under a group life certificate which meet

the conditions defined in VM-20, Section 1.B, and that are not included in either (a) or (b).

Guidance Note:

(i) Definitions of preneed and guaranteed issue insurance policy are in VM-01.

(ii) For statements of exemption filed for calendar year 2022 and beyond, the amount in subsection 2.e

was reported in the prior calendar year life/health annual statement, VM-20 Reserve Supplement, Part

2, if applicable.

3. Policies and Certificates Excluded from the Life PBR Exemption:

a. Universal life with secondary guarantee (ULSG) policies or certificates, or policies or certificates

– other than ULSG – that contain a rider with a secondary guarantee, in which the secondary

guarantee does not meet the VM-01 definition of a “non-material secondary guarantee.”

4. Each exemption, or lack of an exemption, outlined in D. subsection 1.G.1 – D. subsection 1.G.3 above

applies only to policies or certificates issued or assumed in the current year, and it applies to all future

valuation dates for those policies or certificates. However, if policies or certificates did not qualify for

the Life PBR Exemption during the year of issue but would have qualified for the Life PBR Exemption

if the current Valuation Manual requirements had been in effect during the year of issue, then the

domiciliary commissioner may allow an exemption for such policies or certificates. The minimum

reserve requirements for the ordinary life policies, including individual certificates under group life

contracts which meet all the requirements in VM-20 Section 1.B, subject to the exemption are those

pursuant to applicable methods required in VM-A and VM-C using the mortality as defined in VM-

20 Section 3.C.1 and VM-M Section 1.H.

VM Change 4 – VM-20: Requirements for Principle-Based Reserves for Life Products

VM-20: Requirements for Principles-Based Reserves for Life Products

Section 1: Purpose

A. These requirements establish the minimum reserve valuation standard for individual life insurance policies

issued on or after the operative date of the Valuation Manual and subject to a principle-based valuation

with an NPR floor under Model #820. These requirements constitute the Commissioners Reserve Valuation

Method (CRVM) for policies of individual life insurance.

© 2021 National Association of Insurance Commissioners

7

© 2010 National Association of Insurance Commissioners 6

B. Individual life certificates under a group life contract shall be subject to the requirements of VM-20 if all

of the following are met. These requirements constitute the Commissioners Reserve Valuation Method

(CRVM) for such certificates.

1. An individual risk selection process, defined as follows, is used to obtain group life insurance

coverage;

An individual risk selection process is one that is based on characteristics of the insured(s) beyond sex,

gender, age, tobacco usage, and membership in a particular group. This may include, but is not limited to,

completion of an application (beyond acknowledgement of membership to the group, sex, gender and age),

questionnaire(s), online health history or tele-interview to obtain non-medical and medical or health history

information, prescription history information, avocations, usage of tobacco, family history, or submission

of fluids such as blood, Home Office Specimens (HOS), or oral fluid. The resulting risk classification is

determined based on the characteristics of the individual insured(s) rather than the group, if any, of which

it is a member (e.g., employer, affinity, etc.). The individual certificate holder is charged a premium rate

based solely on the individual risk selection process and not on membership in a specific group.

2. The individual certificates utilize premiums or cost of insurance schedules and charges based on

the individual applicant’s issue age, duration from underwriting, coverage amount and risk classification

and there is a stated or implied schedule of maximum gross premiums or net cash surrender value required

in order to continue coverage in force for a period in excess of one year;

3. The group master contract is designed, priced, solicited, and managed similar to individual ordinary

life insurance policies rather than specific to the group as a whole;

4. The individual certificates have similar acquisition approaches, provisions, certificate-holder

rights, pricing, and risk classification to individual ordinary life insurance contracts.

5. The individual certificates are issued on or after the operative date of the Valuation Manual except

election of the transition period in Section 2, subsection 1.F.1.

Guidance Note: The use of evidence of insurability does not by itself constitute an individual risk

selection process. Use of information obtained from a census or question(s) regarding gender,

occupation, age, income and/or tobacco usage solely for purposes of determining a rate classification

does not by itself qualify a group as having used an individual risk selection process. Group insurance

where the underwriting based on the characteristics of the group and census data but where some

individuals are subjected to individual risk selection as a result of compensation level, age, an existing

medical condition or impairment, late entry into the group, failure of the group to meet minimum

participation requirements or voluntary buy-up of increased coverage does not meet the definition of an

individual risk selection process.

Guidance Note: Coverage amount does not imply a requirement for banding of premiums or

charges but rather rates or charges that are multiplied by number of units of coverage of face

amount (or net amount at risk) per $1,000 to obtain the actual premium or charge.

© 2021 National Association of Insurance Commissioners

8

© 2010 National Association of Insurance Commissioners 7

VM Change 5 - VM-20: Requirements for Principle-Based Reserves for Life Products

Section 2: Minimum Reserve

A. All policies subject to these requirements shall be included in one of the VM-20 Reserving

Categories, as specified in Section 2.A.1, Section 2.A.2 and Section 2.A.3 below.

Guidance Note: Since group insurance subject to an individual risk selection process and meeting all

the requirements in Section 1.B is subject to VM-20 requirements, Section 2.A shall apply—meaning

that any such contracts will be included in one of the VM-20 Reserving Categories defined by Section

2.A.1, Section 2.A.2, and 2.A.3. All requirements in VM-31 which apply to a VM-20 Reserving

Category shall apply to any group insurance subject to individual risk selection that has been included

in that VM-20 Reserving Category.

The company may elect to exclude one or more groups of policies from the stochastic reserve

calculation and/or the deterministic reserve calculation. When excluding a group of policies from a

reserve calculation, the company must document that the applicable exclusion test defined in Section 6

is passed for that group of policies. The minimum reserve for each VM-20 Reserving Category is

defined by Section 2.A.1, Section 2.A.2 and Section 2.A.3, and the total minimum reserve equals the

sum of the Section 2.A.1, Section 2.A.2 and Section 2.A.3 results below, defined as:

© 2021 National Association of Insurance Commissioners

9

© 2010 National Association of Insurance Commissioners 8

VM Change 6 – VM-20 Reserves Supplement, Part 2: Life PBR Exemption

Refer to NAIC Blanks (E) Working Group, request for modification to the supplemental report for the Life PBR

Exemption, to show the premiums for group life that utilized an individual risk selection process and meets all of

the requirements in VM-20 Section 1.B. as these premiums are currently grouped together with other group

insurance in Exhibit 1. As there are other instances where the ordinary life premiums are not included in the

determination of the Life PBR Exemption (e.g., for guaranteed issue policies), it may be useful to request addition

of the breakdown of premiums used to determine the exemption.

Possible insertion

between questions 1

and 2 for disclosure

of premiums used in

the determination of

eligibility for the

Life PBR

exemption, split by

ordinary life and

group subject to an

individual risk

selection process

and meeting all of

the requirements in

VM-20 Section 1.B.

© 2021 National Association of Insurance Commissioners

10

Life Actuarial (A) Task Force/ Health Actuarial

(B) Task Force

Amendment Proposal Form

1. Identify yourself, your affiliation and a very brief description (title) of the issue.

Joint submission by NAIC staff and Staff of Office of Principle-Based Reserving, California Department

of Insurance – Clarify areas of confusion relating to the topic of materiality.

2. Identify the document, including the date if the document is “released for comment,” and

the location in the document where the amendment is proposed:

Valuation Manual (January 1, 2021 edition), VM-20 Section 2.H, new Section 2.I, and Section 7.E.1.g

3. Show what changes are needed by providing a red-line version of the original verbiage with

deletions and identify the verbiage to be deleted, inserted or changed by providing a red-line

(turn on “track changes” in Word®) version of the verbiage. (You may do this through an

attachment.)

See attached Appendix.

4. State the reason for the proposed amendment? (You may do this through an attachment.)

See attached Appendix.

.

NAIC Staff Comments:

Dates: Received

Reviewed by Staff

Distributed

Considered

09/21/20

RM

APF 2020-02 rev. 09/21/20

W:\National Meetings\2010\...\TF\LHA\

© 2015 National Association of Insurance Commissioners

© 2021 National Association of Insurance Commissioners

11

Appendix

ISSUE:

Skipping steps in VM-20 is not allowed on grounds of immateriality. Some companies are skipping

some VM-20 requirements altogether, without providing a simplification, approximation, or modeling

technique that satisfies the VM-20 Section 2.G requirement that such simplifications neither materially

understate nor downwardly bias the reserves. Simply skipping portions of the requirements, such as not

computing an NPR, or not computing the DR and/or SR when exclusion tests have not been performed,

inherently bias the reserve downward since their omission can only be neutral or decrease the resulting

reserve. Without computing even a simplified model for Section 2.G analysis that shows there is not a

decrease in the final reserve, this makes the skipping of the step violate Section 2.G. This APF clarifies

that these types of omissions are not allowed. This has always been the case, but perhaps needs more

emphasis in the Valuation Manual.

SECTION:

VM-20 Section 2.H and new Section 2.I, and VM-20 Section 7.E.1.g

REDLINE:

VM-20 Section 2.H

H. The company shall establish, for the DR and SR, a standard containing the criteria for

determining whether an assumption, risk factor or other element of the principle-based

valuation has a material impact on the size of the reserve. This standard shall be applied

when identifying material risks under VM-20 Section 9.B.1. Such a standard shall also

apply to the NPR with respect to VM-20 Section 2.G.

Guidance Note:

For example, the standard may be expressed as an impact of more than X dollars or Y% of the

reserve, whichever is greater, where X and Y are chosen in a manner that is meant to stand the test

of time and not need periodic revision.

The standard is based on the impact relative to the size of the NPR, DR and SR as opposed to the

impact relative to the overall financial statement (e.g., total company reserves or surplus).

Reviewing items that may lead to a material misstatement of the financial statement in the current

year is appropriate in its own context, but it is not appropriate for identifying material risks for

PBR, which itself is an emerging risk.

Note that the criteria apply to the NPR, DR and SR, and not just the final reported reserve. For

example, if the DR is less than the NPR, the criteria still apply to the DR.

The standard also applies to exclusion tests, as they are an element of the principle-based valuation.

© 2021 National Association of Insurance Commissioners

12

(new) VM-20 Section 2.I

I. Section 2.G and Section 2.H provide companies some flexibility in assumption setting and

modeling methodologies, but they do not allow for skipping mandated steps without

providing a valid approximation, simplification, or modeling technique under Section 2.G

that neither materially understates nor downwardly biases the reserve.

Examples of omissions that would not satisfy VM-20 Section 2.G: not computing even a

simplified NPR, not computing even a simplified DR or SR without having passed the

relevant exclusion test(s), omitting prescribed mortality margins, not establishing any lapse

margins, not building even a simplified asset model for the DR, using the alternative

investment strategy without first determining that it produces a higher reserve than the

company investment strategy, and ignoring post-level term losses.

Guidance Note: The issue here is not the use of approximations; it is about skipping mandated

VM-20 requirements. Thus, for example, this does not rule out the use of a relatively simple

asset model that is acceptable pursuant to VM-20 Section 7.E.1.a, nor the judicious use of the

previous year’s assumption development work to save time and effort.

VM-20 Section 7.E.1.g Guidance Note

Guidance Note: VM-31 requires a demonstration of compliance with VM-20 Section 7.E.1.g. In

many cases, particularly if the model investment strategy does not involve callable assets, it is

expected that the demonstration of compliance will not require running the reserve calculation

twice. For example, an analysis of the weighted average net reinvestment spread on new

purchases by projection year (gross spread minus prescribed default costs minus investment

expenses) of the model investment strategy compared to the weighted average net reinvestment

spreads by projection year of the alternative strategy may suffice. The assumed mix of asset

types, asset credit quality or the levels of non-prescribed spreads for other fixed income

investments may need to be adjusted to achieve compliance. Or, the company may be able to rely

on a previous year’s determination as to which strategy produces a higher reserve, if the assets

and strategy have not changed very substantially since then.

© 2021 National Association of Insurance Commissioners

13

REASONING:

Some companies have mistakenly believed that it was permissible to skip certain significant steps

outlined in VM-20, without using a valid approximation or simplification that they have shown does not

materially understate or bias reserves in a downward direction.

Note: Comment letters were received on an earlier draft of this APF, in response to which this newer

version has eliminated any mention of PIMR and has made it clearer that a simplified asset model may

in some circumstances be acceptable and that a full-blown run of both the actual investment strategy

and the alternative investment strategy is not necessarily something that has to be done every year.

© 2021 National Association of Insurance Commissioners

14

Dates: Received

Reviewed by Staff

Distributed

Considered

2/18/20

RM

Notes: APF 2020-03 revised 2/26/20 Exposed 2/27/20, Revised 3/31/20

Life Actuarial (A) Task Force/ Health Actuarial (B) Task Force

Amendment Proposal Form*

1. Identify yourself, your affiliation and a very brief description (title) of the issue.

Identification:

Rachel Hemphill, Texas Department of Insurance

Title of the Issue:

Clarify NPR calculation requirements.

2. Identify the document, including the date if the document is “released for comment,” and the location in

the document where the amendment is proposed:

VM-20 Section 3.B.1 – 3.B.3, and VM-20 Section 3.B.6.d.i

January 1, 2020 NAIC Valuation Manual

3. Show what changes are needed by providing a red-line version of the original verbiage with deletions and

identify the verbiage to be deleted, inserted or changed by providing a red-line (turn on “track changes” in

Word®) version of the verbiage. (You may do this through an attachment.)

See attached.

4. State the reason for the proposed amendment? (You may do this through an attachment.)

Clarify any confusion on whether more direct calculations of the NPR to reflect non-annual premium

modes, etc., are allowed. The current guidance note in Section 3.B.3 states that these may be reflected

either “directly or through adjusting accounting entries”. However, due to some confusion on this point, I

suggest emphasizing that more direct calculation methods are not prohibited. This is consistent with SSAP

51R, Paragraph 24:

24. Since terminal reserves are computed as of the end of a policy year and not the reporting date,

the terminal reserve as of policy anniversaries immediately prior and subsequent to the reporting

date are adjusted to reflect that portion of the net premium that is unearned at the reporting date.

© 2021 National Association of Insurance Commissioners

15

© 2010 National Association of Insurance Commissioners 1

This is generally accomplished using either the mean reserve method or the mid-terminal method

as discussed in paragraphs 25-28. Other appropriate methods, including an exact reserve

valuation, may also be used.

For re-exposure, to address both the question posed in the initial exposure of clearly reflecting both mean

and mid-terminal adjustments, as well as to address comments received, I recommend language consistent

with SSAP 51R, paragraph 24. SSAP 51R paragraphs 25-28 are referenced by paragraph 24. They are

provided below for completeness, and specific references for policies subject to the Valuation Manual are

highlighted.

Mean Reserve Method

25. Under the mean reserve method, the policy reserve equals the average of the terminal reserve

at the end of the policy year and the initial reserve (the initial reserve is equal to the previous year’s

terminal reserve plus the net annual valuation premium for the current policy year). When reserves

are calculated on the mean reserve basis, it is assumed that the net premium for a policy is collected

annually at the beginning of the policy year and that policies are issued ratably over the calendar

year.

26. However, as premiums are often received in installments more frequently than annually and

since the calculation of mean reserves assumes payment of the current policy year’s entire net

annual premium, the policy reserve is overstated by the amount of net modal premiums not yet

received for the current policy year as of the valuation date. As a result, it is necessary to compute

and report a special asset to offset the overstatement of the policy reserve.

27. This special asset is termed “deferred premiums.” Deferred premiums are computed by taking

the gross premium (or premiums) extending from (and including) the modal (monthly, quarterly,

semiannual) premium due date or dates following the valuation date to the next policy anniversary

date and subtracting any such deferred premiums that have actually been collected. Deferred

premium assets shall also be reduced by loading. Since the calculation of mean reserves assumes

payment of the current policy year’s entire net annual premium, deferred premium assets are

considered admitted assets to compensate for the overstatement of the policy reserve. For policies

subject to the Valuation Manual requirements, the deferred premium asset will continue to be

calculated for the net premium reserve component of the total principle-based reserve.

Mid-Terminal Method

28. Under the mid-terminal method, the policy reserves are calculated as the average of the

terminal reserves on the previous and the next policy anniversaries. These reserves shall be

accompanied by an unearned premium reserve consisting of the portion of valuation premiums

paid or due covering the period from the valuation date to the next policy anniversary date. For

policies subject to the Valuation Manual requirements, the adjustment to the unearned premium

reserve will continue to be calculated for the net premium reserve component of the total principle-

based reserve.

Since the guidance note at the end of Section 3.B.3 contains requirements and not just guidance, it should

be taken out of a guidance note. This requires moving the four terms to Section 3.B.1 and updating two

cross references in VM-20 Section 3.B.6.d.i.

* This form is not intended for minor corrections, such as formatting, grammar, cross–references or spelling. Those types of changes do not require action by

the entire group and may be submitted via letter or email to the NAIC staff support person for the NAIC group where the document originated.

NAIC Staff Comments:

W:\National Meetings\2010\...\TF\LHA\

© 2021 National Association of Insurance Commissioners

16

© 2010 National Association of Insurance Commissioners 2

VM-20 Section 3.B.1 – 3.B.3

B. NPR Calculation

1. For the purposes of Section 3, the following terms apply:

a. A policy with “multiple secondary guarantees” is one that: a) simultaneously has more than

one shadow account; b) simultaneously has more than one cumulative premium type of

guarantee; or c) simultaneously has at least one of each. A single shadow account with a variety

of possible end dates to the secondary guarantee, depending on the policyholder’s choice of

funding level, constitutes a single—not multiple—secondary guarantee.

Guidance Note:

Policy designs that are created simply to disguise guarantees or exploit a perceived loophole must

be treated in a manner similar to more typical product designs with similar guarantees. If a policy

contains multiple secondary guarantees, such that a subset of those secondary guarantees in

combination represent an implicit guarantee that would produce a higher NPR if that implicit

guarantee were treated as an explicit secondary guarantee of the policy, then the policy should be

treated as if that implicit guarantee were an explicit guarantee. For example, if there were a policy

with a “sequential secondary guarantee” where only one secondary guarantee applied at any given

point in time but with a series of secondary guarantees strung together with one period ending when

the next one began, the combined terms of the secondary guarantees would be regarded as a single

secondary guarantee.

b. The “fully funded secondary guarantee” at any time is:

i. For a shadow account secondary guarantee, the minimum shadow account fund value

necessary to fully fund the secondary guarantee for the policy at that time. For any policy

for which the secondary guarantee contractually cannot be fully funded in advance, this

shall be the present value of the contractually permitted premium stream that would fully

fund the guarantee at the earliest possible date (using the valuation interest rate and

mortality standard specified in Section 3.C).

ii. For a cumulative premium secondary guarantee, the amount of cumulative premiums

required to have been paid to that time that would result in no future premium requirements

to fully fund the guarantee, accumulated with any interest or accumulation factors per the

contract provisions for the secondary guarantee. For any policy for which the secondary

guarantee contractually cannot be fully funded in advance, this shall be the present value

of the contractually permitted premium stream that would fully fund the guarantee at the

earliest possible date (using the valuation interest rate and mortality standard specified in

Section 3.C).

c. The “actual secondary guarantee” at any time is:

i. For a shadow account secondary guarantee, the actual shadow account fund value at that

time.

ii. For a cumulative premium secondary guarantee, the actual premiums paid to that point

in time, accumulated with any interest or accumulation factors per the contract provisions

for the secondary guarantee.

d. The “level secondary guarantee” at any time is:

i. For a shadow account secondary guarantee, the shadow account fund value that would

have existed at that time assuming payment of the level gross premium determined

according to Section 3.B.6.c.i.

Deleted: For purposes of this section, a

Formatted: Numbered + Level: 2 + Numbering Style: a, b,

c, … + S

tart at: 1 + Alignment: Left + Aligned at: 1" +

Indent at: 1.25"

Deleted: For the purposes of Section 3, the following terms

apply: …

Formatted: Numbered + Level: 1 + Numbering Style: a, b,

c, … + S

tart at: 2 + Alignment: Left + Aligned at: 1" +

Indent at: 1.25"

Deleted: a.

Deleted: b.

Formatted: Numbered + Level: 1 + Numbering Style: a, b,

c, … + S

tart at: 2 + Alignment: Left + Aligned at: 1" +

Indent at: 1.25"

Deleted: a.

Deleted: b.

Formatted: Numbered + Level: 1 + Numbering Style: a, b,

c, … + S

tart at: 2 + Alignment: Left + Aligned at: 1" +

Indent at: 1.25"

Deleted: a.

© 2021 National Association of Insurance Commissioners

17

© 2010 National Association of Insurance Commissioners 3

ii. For a cumulative premium secondary guarantee, the amount of cumulative level gross

premiums determined according to Section 3.B.6.c.i, accumulated with any interest or

accumulation factors per the contract provisions for the secondary guarantee.

2. Section 3.B.4, Section 3.B.5 and Section 3.B.6 provide the calculation of a terminal NPR under

the assumption of an annual mode gross premium. In Section 3.B.4, Section 3.B.5 and Section

3.B.6, the gross premium referenced is the gross premium for the policy assuming an annual

premium mode.

3. Since terminal NPRs are computed as of the end of a policy year and not the reporting date, the

terminal NPR as of policy anniversaries immediately prior and subsequent to the reporting date

are adjusted to reflect that portion of the net premium that is unearned at the reporting date.

This is generally accomplished using either the mean reserve method or the mid-terminal

method as discussed in SSAP 51R. Other appropriate methods, including an exact reserve

valuation, may also be used.

VM-20 Section 3.B.6.d.i

As of the valuation date for the policy being valued, determine the actual secondary guarantee, denoted ASGx+t,

as outlined in Section 3.B.1.c and the fully funded secondary guarantee, denoted FFSGx+t, as outlined in Section

3.B.1.b.

Deleted: b.

Moved (insertion) [1]

Deleted: The definition of the NPR in

Formatted: Numbered + Level: 1 + Numbering Style: 1, 2,

3, … + S

tart at: 2 + Alignment: Left + Aligned at: 1" +

Indent at: 1.25"

Deleted: is intended to result in

Deleted: T

Deleted: should be

Formatted: Numbered + Level: 1 + Numbering Style: 1, 2,

3, … + S

tart at: 2 + Alignment: Left + Aligned at: 1" +

Indent at: 1.25"

Deleted: Guidance Note:

Moved up [1]: The definition of the NPR in Section 3.B.4,

Section 3.B.5 and Section 3.B.6 is intended to result in a terminal

NPR under the assumption of an annual mode gross premium.

The gross premium referenced should be the gross premium for

the policy assuming an annual premium mode.

Deleted:

The reported reserve as of any valuation date should

reflect the actual premium mode for the policy and the actual

valuation date relative to the policy issue date either directly or

through adjusting accounting entries.

Deleted: 2

© 2021 National Association of Insurance Commissioners

18

Dates: Received

Reviewed by Staff

Distributed

Considered

09/23/20

RM

APF 2020-08

© 2020 National Association of Insurance Commissioners

Life Actuarial (A) Task Force/ Health Actuarial (B) Task Force

Amendment Proposal Form

1. Identify yourself, your affiliation and a very brief description (title) of the issue.

Tim Cardinal, FSA, MAAA, CERA. Cardinalis 1 Consulting.

Clarify and introduce a third permissible technique for the calculation of company experience rates.

2. Identify the document, including the date if the document is “released for comment,” and

the location in the document where the amendment is proposed:

2020 Edition – Valuation Manual, VM-20 Section 9.C.2.d.vi.

3. Show what changes are needed by providing a red-line version of the original verbiage with

deletions and identify the verbiage to be deleted, inserted or changed by providing a red-line

(turn on “track changes” in Word®) version of the verbiage. (You may do this through an

attachment.)

See attached Appendix.

4. State the reason for the proposed amendment? (You may do this through an attachment.)

See attached Appendix and Excel file.

© 2021 National Association of Insurance Commissioners

19

Appendix

SECTION:

VM-20 Section 9.C.2.d.vi.

REDLINE:

9.C.2.d.vi. If the company uses the aggregate company experience for a group of mortality segments

when determining the company experience mortality rates for each of the individual

mortality segments in the group, the company shalluse one of the following methods:

a. Use techniques to further subdivide the aggregate experience into the various mortality

segments (e.g., start with aggregate non-smoker and then use the conservation of total

deaths principle, normalization or other approach to divide the aggregate mortality into

super preferred, preferred and residual standard non-smoker class assumptions).

b. Use techniques to adjust the experience of each mortality segment in the group to

reflect the aggregate company experience for the group (e.g., by credibility weighting

the individual mortality segment experience with the aggregate company experience for

the group).

c. Use a two-step sequential method, which

1) forms subgroups which are groups of mortality segments and are subsets of the

aggregate class of mortality segments being aggregated,

2) uses techniques as in (b) to adjust the experience of each subgroup from (1) to

reflect the aggregate company experience for the group and conserve deaths, and

3) finally, uses techniques as in (a) to further subdivide the subgroups’ adjusted

experience from (2) into the various mortality segments while conserving each

subgroup’s deaths determined in step (2)’s conservation of deaths.

For example, if mortality segments vary by sex, risk class, and face bands, then

1) segments that differ by face band are aggregated to form subgroups that vary

just by sex and risk class,

2) the subgroups’ mortality experience is credibility weighted with the aggregate

company experience for the group and normalized, and

3) the subgroups’ adjusted mortality experience are then subdivided into the

various mortality segments based on credible, external face band relativities and

conservation of deaths is applied to each subgroup’s normalized deaths

determined in (2).

REASONING:

A minor point is clarity. “Either” can mean one or both. The intent is one of a) or b) but not both. The

major issue is both a) and b) have weaknesses in contexts with high levels of granularity resulting in a

large number of mortality segments such as 120 or 360 segments. For example consider a block with

360 mortality segments determined by 2 sexes × 6 risk classes × 5 face bands × 3 product types × 2

underwriting types (such as full and accelerated). A company may have very high credibility for each of

12 segments as determined by 2 sexes × 6 risk classes but have very low credibility for each of the 360

segments. Both a) and b) could produce company experience rates that negate the very reasons a

company uses a high level of granularity. Using b) for example, all segment rates would be equal to the

aggregate A/E rates, which is equivalent to no granularity. By applying b) to subgroups and applying a) to

divide the subgroups, the proposed technique c) is more robust drawing upon a) and b)’s strengths

Deleted: either

© 2021 National Association of Insurance Commissioners

20

while mitigating their weakness. If there is one subgroup which is the aggregate then a) is a special case

of c). If each subgroup is a segment then b) is a special case of c). See the attached excel file that adds

two examples to the NAIC examples for a) and b). Example 8 is an example of a correct way to apply c)

and Example 9 is an incorrect way.

© 2021 National Association of Insurance Commissioners

21

Dates: Received

Reviewed by Staff

Distributed

Considered

Notes: APF 2020-09 v.6 (with editorial changes added at time of adoption)

Adopted 11/5/20

Life Actuarial (A) Task Force/ Health Actuarial (B) Task Force

Amendment Proposal Form*

1. Identify yourself, your affiliation and a very brief description (title) of the issue.

Identification:

Rachel Hemphill, Texas Department of Insurance

Title of the Issue:

1. Modify Life PBR Exemption to not require annual exemption requests if the company continues to

meet the premium thresholds and does not have any ULSG with material SG.

2. Not require VM-20 when all new issues arise due to policyholders exercising guarantees or options

(e.g. for conversion) in existing policies valued under VM-A/VM-C.

2. Identify the document, including the date if the document is “released for comment,” and the location in

the document where the amendment is proposed:

Valuation Manual Section II, Subsection 1.D

January 1, 2020 NAIC Valuation Manual

3. Show what changes are needed by providing a red-line version of the original verbiage with deletions and

identify the verbiage to be deleted, inserted or changed by providing a red-line (turn on “track changes” in

Word®) version of the verbiage. (You may do this through an attachment.)

See attached.

4. State the reason for the proposed amendment? (You may do this through an attachment.)

Reduce filing burden for companies and state regulators by making the Life PBR Exemption a one-time

filing until conditions for the exemption change. Allow exemption for companies that do not meet the

premium thresholds, but are only issuing new policies that would be subject to VM-20 due to policyholders

exercising guarantees or options (e.g. for conversion) from existing policies being valued under the pre-

PBR framework.

* This form is not intended for minor corrections, such as formatting, grammar, cross–references or spelling. Those types of changes do not require action by

the entire group and may be submitted via letter or email to the NAIC staff support person for the NAIC group where the document originated.

NAIC Staff Comments:

W:\National Meetings\2010\...\TF\LHA\

© 2021 National Association of Insurance Commissioners

22

© 2010 National Association of Insurance Commissioners 1

Valuation Manual Section II, Subsection 1.D

D. Life PBR Exemption

1. A company meeting at least one of the conditions in D.2 below may file a statement of exemption for

ordinary life insurance policies, except for policies in D.3 below, issued directly or assumed during the

current calendar year, that would otherwise be subject to VM-20. If a company has no business issued

directly or assumed during the current calendar year that would otherwise be subject to VM-20, a statement

of exemption is not required. For a filed statement of exemption, the statement must be filed with the

domiciliary commissioner prior to July 1 of that year certifying that at least one of the two conditions in

D.2 was met and the statement of exemption must also be included with the NAIC filing for the second

quarter of that year.

The domiciliary commissioner may reject such statement prior to Sept. 1 and require the company to follow

the requirements of VM-20 for the ordinary life policies covered by the statement.

If a filed statement of exemption is not rejected by the domiciliary commissioner, the filing of subsequent

statements of exemption is not required as long as the company continues to qualify for the exemption;

rather, ongoing statements of exemption for each new calendar year will be deemed to not be rejected,

unless: 1) the company fails to meet either condition in D.2 below, 2) the policies contain those in D.3

below, or 3) the domiciliary commissioner contacts the company prior to Sept. 1 and notifies them that the

statement of exemption is rejected. If any of these three events occur, then the statement of exemption for

the current calendar year is rejected and a new statement of exemption must be filed and not rejected in

order for the company to exempt additional policies. In the case of an ongoing statement of exemption,

rather than include a statement of exemption with the NAIC filing for the second quarter of that year, the

company should enter “SEE EXPLANATION” in response to the Life PBR Exemption supplemental

interrogatory and provide as an explanation that the company is utilizing an ongoing statement of

exemption.

2. Conditions for Exemption:

a. The company has less than $300 million of ordinary life premiums

1

, and if the company is a member

of an NAIC group of life insurers, the group has combined ordinary life premiums

1

of less than $600

million; or

b. The only new policies subject to VM-20 being issued or assumed by the company are due to election

of policy benefits or features from existing policies that are being valued under VM-A and VM-C and

the company was exempted from, or otherwise not subject to, the requirements of VM-20 in the prior

year.

3. Policies Excluded from the Life PBR Exemption:

a. Universal life with secondary guarantee (ULSG) policies with a secondary guarantee that does not meet

the VM-01, Definitions for Terms in Requirements, definition of a “non-material secondary guarantee.”

4. Each exemption, or lack of an exemption, applies only to policies issued or assumed in the current year,

and it applies to all future valuation dates for those policies. The minimum reserve requirements for the

ordinary life policies subject to the exemption are those pursuant to applicable methods required in VM-A

and VM-C using the mortality as defined in VM-20 Section 3.C.1 and VM-M Section 1.H.

Valuation Manual Section II, Subsection 1.D - Footnote

1

Premiums are measured as total (first year, single, and renewal) direct plus total (first year, single, and

renewal) reinsurance assumed from an unaffiliated company from the ordinary life line of business reported

in the prior calendar year life/health annual financial statement, Exhibit 1, Part 1, Column 3, “Ordinary Life

Insurance” excluding premiums for guaranteed issue policies and preneed life contracts and excluding

amounts that represent the transfer of reserves in force as of the effective date of a reinsurance assumed

Deleted: the

Deleted: Such a

Deleted: based on premiums from the prior calendar year

annual statement

Deleted: . T

Deleted: .

© 2021 National Association of Insurance Commissioners

23

© 2010 National Association of Insurance Commissioners 2

transaction and are reported in Exhibit 1 Part 1, Column 3 as ordinary life insurance premium. Preneed is

as defined in VM-01.

© 2021 National Association of Insurance Commissioners

24

Life Actuarial (A) Task Force

Amendment Proposal Form 2020-10

Exposed for a 12-day public comment period ending June 7, 2021

Request for Comment: During the exposure, commenters are specifically asked to address the

four versions exposed for the handling of YRT for the 2017-2019 issue years.

Please submit comments to Reggie Mazyck (RMazyck@naic.org

) by COB 5/25/21.

© 2021 National Association of Insurance Commissioners

25

Dates: Received

Reviewed by Staff

Distributed

Considered

RM

APF 2020-10 exposed 5/27/21 with non-substantive revision

© 2015 National Association of Insurance Commissioners

Life Actuarial (A) Task Force/ Health Actuarial

(B) Task Force

Amendment Proposal Form

1. Identify yourself, your affiliation and a very brief description (title) of the issue.

Pat Allison – NAIC, Scott O’Neal – NAIC, Mary Bahna-Nolan – Pacific Life, and Rachel Hemphill – Texas

Department of Insurance; SOA for development of rates and loading.

Reflect a prudent level of mortality improvement beyond the valuation date.

2. Identify the document, including the date if the document is “released for comment,” and the

location in the document where the amendment is proposed:

Valuation Manual (January 1, 2021 edition), VM-20 Section 6.A.2.b.v, VM-20 Section 8.C

Introductory Paragraph, VM-20 Section 8.C.18 and Guidance Note, VM-20 Section 9.C.2.h, VM-20

Section 9.C.3.g, VM-20 Section 9.C.7.a, VM-20 Section 9.C.7.h (new), VM-31 Section 3.D.8.g (new –

for 2017-2019 YRT Version 3 only), VM-31 Section 3.D.3.i, VM-31 Section 3.D.8.g (2017-2019 YRT

handling option 3 only, new reporting section), VM-31 Section 3.D.11.c.i

3. Show what changes are needed by providing a red-line version of the original verbiage with

deletions and identify the verbiage to be deleted, inserted or changed by providing a red-line

(turn on “track changes” in Word®) version of the verbiage. (You may do this through an

attachment.)

See attached Appendix.

4. State the reason for the proposed amendment? (You may do this through an attachment.)

We propose to reflect a prudent level of mortality improvement beyond the valuation date, using

SOA analysis for best estimate future mortality improvement and margin. The requirements also

need to be clarified for the handling of historical or anticipated future mortality deterioration (i.e.,

negative improvement).

With the reflection of a prudent level of future mortality improvement in the mortality assumption,

the interim 1/2cx approach to YRT is a reasonable consideration for a long-term approach.

For LATF consideration for re-exposure, there are four versions of the handling of the 2017-2019

issue year carveout from the interim YRT solution: 1) the original exposure, removing the carveout

with the 1/2cx being made a longer term approach, 2) a modified version that removes the

carveout, but makes that removal contingent on the first set of SOA future mortality rates being

adopted, in case of delay, 3) a modified version that removes the carveout, but allows for a phase-

in of the effect of this change, and 4) a version making the carveout long-term. These versions are

presented starting on Page 6 of this document, after the other edits which do not vary based on

this options.

© 2021 National Association of Insurance Commissioners

26

© 2015 National Association of Insurance Commissioners

Appendix

VM-20 Section 6.A.2.b.v:

v. Anticipated mortality improvement beyond the projection start date shall be reflected in the

mortality assumption for the purpose of calculating the stochastic exclusion ratio. The future

mortality improvement factors shall be no greater than the unloaded factors determined by the SOA,

adopted by LATF, and published on the SOA website, at [link/reference to SOA site TBD].

Guidance Note: Mortality improvement may be positive or negative (i.e., deterioration). The anticipated

mortality improvement may be lower than the rates published by the SOA, for example, if the company’s

best estimate for mortality improvement for a particular block, such as simplified issue, is lower. Prior to

adoption by LATF of the first set of future mortality improvement factors, the future mortality improvement

rates shall be 0%.

To allow time for companies to reflect the updated mortality improvement rates, the rates that are

to be used in the year-end YYYY valuation should be adopted by LATF and published on the SOA

website by September of YYYY. If this timeline is not met, then at the company’s option they may

use the mortality improvement rates for the prior year (year YYYY-1).

VM-20 Section 9.C.2.h:

h. Mortality improvement shall not be incorporated beyond the valuation date in the company experience

mortality rates. However, historical mortality improvement from the central point of the underlying

company experience data to the valuation date may be incorporated.

Guidance Note: Future mortality improvement is not applied to the company experience mortality rates,

since it would be duplicative of the future mortality improvement that is applied to the prudent estimate

assumptions for mortality in Section 9.C.7.f.

VM-20 Section 9.C.3.g:

g. Mortality improvement shall not be incorporated beyond the valuation date in the industry basic table.

However, historical mortality improvement from the date of the industry basic table (e.g., Jan. 1, 2008, for

the 2008 VBT and July 1, 2015, for the 2015 VBT) to the valuation date shall be incorporated using the

improvement factors for the applicable industry basic table as determined by the SOA, adopted by LATF,

and published on the SOA website, https://www.soa.org/research/topics/indiv-val-exp-study-list/

(Mortality Improvement Rates for AG-38 for Year-End YYYY).

Guidance Note: Future mortality improvement is not applied to the industry basic table, since it would be

duplicative of the future mortality improvement that is applied to the prudent estimate assumptions for

mortality in Section 9.C.7.f.

Deleted: M

Deleted: may not

Deleted: the

Deleted: may

© 2021 National Association of Insurance Commissioners

27

© 2015 National Association of Insurance Commissioners

To allow time for companies to reflect the updated mortality improvement rates, the rates that are to be

used in the year-end YYYY valuation should be adopted by LATF and published on the SOA website by

September of YYYY. If this timeline is not met, then at the company’s option they may use the most recent

set of prior mortality improvement rates adopted by LATF and published on the SOA website.

VM-20 Section 9.C.7.a:

If applicable industry basic tables are used in lieu of company experience as the anticipated experience

assumptions, or if the level of credibility of the data as provided in Section 9.C.5 is less than 20%, the

prudent estimate assumptions for each mortality segment shall equal the respective mortality rates in the

applicable industry basic tables as provided in Section 9.C.3, adjusted as necessary pursuant to Section

9.C.7.e and for any applicable improvement pursuant to Section 9.C.3.g, plus the prescribed margin as

provided in Section 9.C.6.c, plus any applicable additional margin pursuant to Section 9.C.6.d.v and/or

Section 9.C.6.d.vi. Future mortality improvement, pursuant to Section 9.C.7.f, shall be applied to the

prudent estimate assumption for mortality.

Section 9.C.7.b.vi:

Beginning in the first policy duration after policy duration E, the prudent estimate mortality assumptions

for each policy in a given mortality segment are determined as a weighted average of the company

experience mortality rates with margins and the applicable industry basic table with margins, in which the

weights on the company rates grade linearly from 100% down to 0%. This grading must be completed—

i.e., must reach 100% of industry table—no later than the beginning of the first policy duration after policy

duration Z (the determination of the applicable industry basic table is described in Section 9.C.3). Thus, the

prudent estimate mortality rate, prior to any adjustments pursuant to Sections 9.C.7.c, 9.C.7.d, 9.C.7.e, and

9.C.7.f below, is:

VM-20 Section 9.C.7.f (new section):

Twenty years of future mortality improvement that the company anticipates beyond the valuation date shall

be applied to the prudent estimate assumptions for mortality, using prudent future mortality improvement

factors no greater than the loaded factors determined by the SOA, adopted by LATF, and published on the

SOA website, at [link/reference to SOA site TBD].

Guidance Note: Mortality improvement may be positive or negative (i.e., deterioration). The anticipated

mortality improvement may be lower than the rates published by the SOA, even zero, for example, if the

company’s best estimate for mortality improvement for a particular block, such as simplified issue, is lower.

Prior to adoption by LATF of the first set of future mortality improvement factors, the future mortality

improvement rates shall be 0%.

To allow time for companies to reflect the updated mortality improvement rates, the rates that are to be

used in the year-end YYYY valuation should be adopted by LATF and published on the SOA website by

September of YYYY. If this timeline is not met, then at the company’s option they may use the mortality

improvement rates for the prior year (year YYYY-1).

Deleted: including

Commented [RH1]: Craig: Section 9.C.7.f needs to be added in

Section 9.C.7.b.vi, as follows: “Thus, the prudent estimate mortality

rate, prior to any adjustments pursuant to Sections 9.C.7.c, 9.C.7.d,

9.C.7.e and 9.C.7.f below, is:”

Deleted: and

© 2021 National Association of Insurance Commissioners

28

© 2015 National Association of Insurance Commissioners

VM-31 Section 3.D.3.i:

i. Mortality Improvement – Description of and rationale for the mortality improvement assumptions

applied up to the valuation date and the mortality improvement assumptions applied beyond the

valuation date. Such a description shall include the assumed start and end dates of the

improvements and a table of the annual improvement percentage(s) used, both without and with

margin, separately for company experience and the industry basic table(s), along with a sample

calculation of the adjustment (e.g., for a male preferred nonsmoker age 45).

VM-31 Section 3.D.11.c.i:

i. If the company believes the method used to determine anticipated experience mortality assumptions

includes an implicit margin, the company can adjust the anticipated experience assumptions to

remove this implicit margin for this reporting purpose only. If any such adjustment is made, the

company shall document the rationale and method used to determine the anticipated experience

assumption.

Deleted: Adjustments for

Deleted: any adjustments to

Deleted: mortality assumptions for

Deleted: . For example, to the extent the company expects

mortality improvement after the valuation date, any such

mortality improvement is an implicit margin and, therefore, is an

acceptable adjustment to the anticipated experience assumptions

© 2021 National Association of Insurance Commissioners

29

© 2015 National Association of Insurance Commissioners

2017-2019 for Long-Term YRT – Version 1:

VM-20 Section 8.C, introductory paragraph:

C. Reflection of Reinsurance Cash Flows in the Deterministic Reserve or Stochastic Reserve

For non-guaranteed YRT reinsurance ceded or assumed, the cash-flow modeling requirements in Sections

8.C.1 through 8.C.14 below do not apply since non-guaranteed YRT reinsurance ceded or assumed does

not need to be modeled; see Section 8.C.18 below. YRT shall include other reinsurance arrangements that

are similar in effect to YRT.

VM-20 Section 8.C.18 and Guidance Note:

18.

When the reinsurance ceded or assumed is on a non-guaranteed YRT or similar basis, the corresponding

reinsurance cash flows do not need to be modeled. Rather, for a ceding company, the post-reinsurance-

ceded DR or SR shall be the pre-reinsurance-ceded DR or SR pursuant to Section 8.D.2, plus any applicable

provision pursuant to Section 8.C.15 and Section 8.C.17, minus the NPR reinsurance credit from Section

8.B. For an assuming company, the DR or SR for the business assumed on a non-guaranteed YRT or similar

basis shall be set equal to the NPR from Section 3.B.8, plus any applicable provision pursuant to Section

8.C.16 and Section 8.C.17. In the case where there are also other reinsurance arrangements that are not on

a non-guaranteed YRT or similar basis, the reinsurance credit shall include the modeled reinsurance credit

reflecting those other reinsurance arrangements. In particular, where there are also other reinsurance

arrangements that are dependent on the non-guaranteed YRT or similar actuarial judgment shall be used to

project cash flows consistent with the above outlined treatment for non-guaranteed YRT or similar

arrangements.

Deleted: For policies issued on or after Jan. 1, 2020, and

optionally for policies issued on or after Jan. 1, 2017, and before Jan.

1, 2020: ¶

¶

Deleted: For policies issued on or after Jan. 1, 2020, and

optionally for policies issued on or after Jan. 1, 2017, and before Jan.

1, 2020:

Deleted: Guidance Note: The above method is an interim

approach. A longer-term solution to YRT is intended to be

adopted by state insurance regulators, after state insurance

regulators and industry have had additional time to consider and

evaluate the variety of approaches that have been put forward as a

potential longer-term solution.¶

© 2021 National Association of Insurance Commissioners

30

© 2015 National Association of Insurance Commissioners

2017-2019 for Long-Term YRT – Version 2:

VM-20 Section 8.C, introductory paragraph:

C. Reflection of Reinsurance Cash Flows in the Deterministic Reserve or Stochastic Reserve

For policies issued on or after Jan. 1, 2020, and optionally for policies issued on or after Jan. 1, 2017, and

before Jan. 1, 2020

up until adoption by LATF of the first set of unloaded future mortality improvement

factors, at which point this shall apply for all policies issued on or after Jan. 1, 2017:

For non-guaranteed YRT reinsurance ceded or assumed, the cash-flow modeling requirements in Sections

8.C.1 through 8.C.14 below do not apply since non-guaranteed YRT reinsurance ceded or assumed does

not need to be modeled; see Section 8.C.18 below. YRT shall include other reinsurance arrangements that

are similar in effect to YRT.

VM-20 Section 8.C.18 and Guidance Note:

18. For policies issued on or after Jan. 1, 2020, and optionally for policies issued on or after Jan. 1, 2017,

and before Jan. 1, 2020 up until adoption by LATF of the first set of unloaded future mortality improvement

factors, at which point this shall apply for all policies issued on or after Jan. 1, 2017:

When the reinsurance ceded or assumed is on a non-guaranteed YRT or similar basis, the corresponding

reinsurance cash flows do not need to be modeled. Rather, for a ceding company, the post-reinsurance-

ceded DR or SR shall be the pre-reinsurance-ceded DR or SR pursuant to Section 8.D.2, plus any applicable

provision pursuant to Section 8.C.15 and Section 8.C.17, minus the NPR reinsurance credit from Section

8.B. For an assuming company, the DR or SR for the business assumed on a non-guaranteed YRT or similar

basis shall be set equal to the NPR from Section 3.B.8, plus any applicable provision pursuant to Section

8.C.16 and Section 8.C.17. In the case where there are also other reinsurance arrangements that are not on

a non-guaranteed YRT or similar basis, the reinsurance credit shall include the modeled reinsurance credit

reflecting those other reinsurance arrangements. In particular, where there are also other reinsurance

arrangements that are dependent on the non-guaranteed YRT or similar actuarial judgment shall be used to

project cash flows consistent with the above outlined treatment for non-guaranteed YRT or similar

arrangements.

Deleted: ¶

Deleted: Guidance Note: The above method is an interim

approach. A longer-term solution to YRT is intended to be

adopted by state insurance regulators, after state insurance

regulators and industry have had additional time to consider and

evaluate the variety of approaches that have been put forward as a

potential longer-term solution.¶

© 2021 National Association of Insurance Commissioners

31

© 2015 National Association of Insurance Commissioners

2017-2019 for Long-Term YRT – Version 3:

C. Reflection of Reinsurance Cash Flows in the Deterministic Reserve or Stochastic Reserve

For non-guaranteed YRT reinsurance ceded or assumed, the cash-flow modeling requirements in Sections

8.C.1 through 8.C.14 below do not apply since non-guaranteed YRT reinsurance ceded or assumed does

not need to be modeled; see Section 8.C.18 below. YRT shall include other reinsurance arrangements that

are similar in effect to YRT.

For policies issued on or after Jan. 1, 2017, and before Jan. 1, 2020, the company may elect, with domiciliary

commissioner approval, a phase-in of the current methodology for non-guaranteed YRT reinsurance with

allowance for future mortality improvement from the methodology in the 2021 Valuation Manual for non-

guaranteed YRT reinsurance without allowance for future mortality improvement, provided that the

company uses a weighted average of the results from the two methodologies, with the weight for the prior

methodology being no more than (20XX-YYYY)/(20XX-2021), where YYYY is the current valuation year

and 20XX is the final year of the phase-in. A company may elect to phase in these requirements over a 3-

year period beginning Jan. 1, 2022 and ending Dec. 31, 2024. A company may elect a longer phase-in

period of up to seven years beginning Jan. 1, 2022 and ending Dec. 31, 2028, with approval of the

domiciliary commissioner.

VM-20 Section 8.C.18 and Guidance Note:

18.

When the reinsurance ceded or assumed is on a non-guaranteed YRT or similar basis, the corresponding

reinsurance cash flows do not need to be modeled. Rather, for a ceding company, the post-reinsurance-

ceded DR or SR shall be the pre-reinsurance-ceded DR or SR pursuant to Section 8.D.2, plus any applicable

provision pursuant to Section 8.C.15 and Section 8.C.17, minus the NPR reinsurance credit from Section

8.B. For an assuming company, the DR or SR for the business assumed on a non-guaranteed YRT or similar

basis shall be set equal to the NPR from Section 3.B.8, plus any applicable provision pursuant to Section

8.C.16 and Section 8.C.17. In the case where there are also other reinsurance arrangements that are not on

a non-guaranteed YRT or similar basis, the reinsurance credit shall include the modeled reinsurance credit

reflecting those other reinsurance arrangements. In particular, where there are also other reinsurance

arrangements that are dependent on the non-guaranteed YRT or similar actuarial judgment shall be used to

project cash flows consistent with the above outlined treatment for non-guaranteed YRT or similar

arrangements.

For policies issued on or after Jan. 1, 2017, and before Jan. 1, 2020, the company may elect, with

domiciliary commissioner approval, a phase-in of the current methodology for non-guaranteed YRT

reinsurance with allowance for future mortality improvement from the methodology in the 2021 Valuation

Manual for non-guaranteed YRT reinsurance without allowance for future mortality improvement,

provided that the company uses a weighted average of the results from the two methodologies, with the